Last week (TFTD: “Know when to Fold‘Em”), we mentioned how busy the news cycle had been, what with riots in LA, another Boeing crash, and speculation of Israeli military action against Iran. The speculation was right on the money, but you couldn’t tell if you were just looking at markets. Yes, oil is markedly higher, but there was little evidence of significant stresses in FX, Equity or Bond markets. Even the shekel showed remarkably little evidence of stress!

Perhaps markets have concluded neither side is interested in closing the Straits of Hormuz. This seems a glass-half-full take. Or perhaps markets are assuming TACO again, although that seems counterintuitive given Trump’s somewhat bellicose public utterances. More plausibly, markets may have decided that Iran is already seeking to de-escalate, given reports that Iranian air defences have suffered significant attrition.

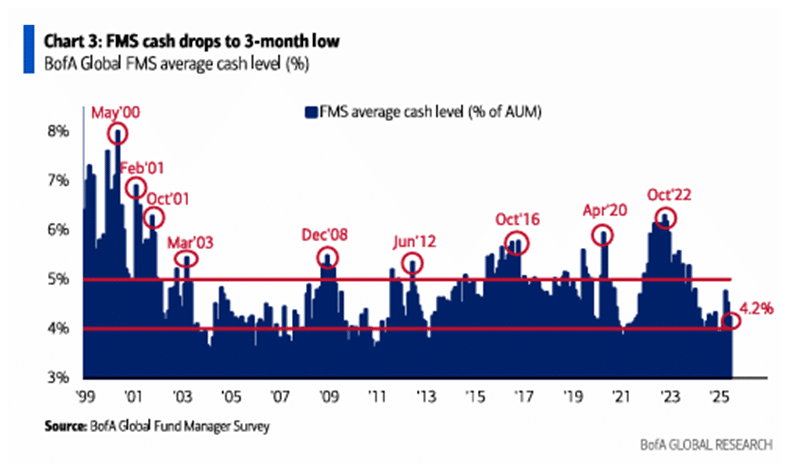

Maybe we are glass-half-empty people, but all these takes seem a little Panglossian to us: not impossible but pretty optimistic. And you could say something similar about the pricing of US equities. Bob Elliot (usually a sober voice) notes that the US consumer is not looking his/her usual robust self. While BoFA FMS noted that cash allocations were at the low end of the range (4.2%), and recession expectations had dropped sharply between April and June. I suppose the point we are trying to make is not that something bad is set to happen, but rather that while risk asset pricing has approached perfection, circumstances seem anything but.

Which is why it was nice to hear Chair Powell’s thoughts on growth and inflation. Market folk like to say “the trend is your friend”, but the trend in the Fed’s inflation and growth outlooks looks anything but friendly. Still, when the FOMC considers these adverse developments, they conclude that while there is no need for unseemly haste, the likely correct course is to reduce rates twice later this year. You might ask how our fearless FOMC officials arrived at that conclusion, but it would be pointless. Beauty is not the only thing in the eye of the beholder; so is the balance of economic risks. But it’s worth noting that even in the contest between Fed Chair and POTUS, the issue is not certain. While Mr. Powell appears to be convinced that rates are appropriate given the uncertainties over the pass-through of tariffs and budget negotiations, the President might still find a way to change his mind. It’s not a lot of fun being a lame duck, and not without costs to the institution. That’s the problem with playing poker with Presidents: they often have cards up their sleeves.