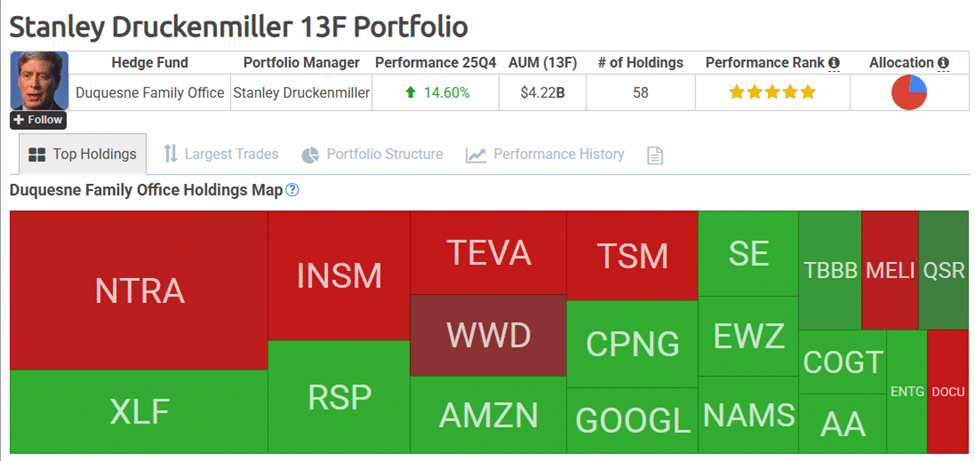

A couple of weeks back, I mentioned the fact that both the Treasury Secretary and the President’s nominee for Fed Chair had both worked with/for Stan Druckenmiller, one of the best speculators of our time. I said that I planned to spend a little more time looking at Mr Druckenmiller’s recent interviews. Naturally, this extends to his recent trades. When it comes to Druckenmiller, Nancy Pelosi, or the inverse Jim Cramer, well, I’m having what they are having! I had assumed it would be hard to follow them, but he’s a prominent guy, and a lot of people watch his trades. Which is how I came across this.

The primary source appears to be a 13F filed by Duquesne, Mr D’s family office, in Q4 2025. So, for all we know, the positions might already have been sold. But I wanted to zero in on two of them. First, EWZ, the Brazil ETF. It’s gratifying to know that Mr D agrees that Brazilian equities are worth a punt.

“Fresh 13F filings out earlier in the week showed that billionaire investor Stanley Druckenmiller’s Duquesne Family Office purchased about 3.5M shares and call options in the iShares MSCI Brazil ETF (EWZ) in Q4 2025, before its 20% year-to-date climb amid a broader rotation away from U.S. growth and a weaker U.S. dollar (DXY). Still, it closed out its stake in the Global X MSCI Argentina ETF (ARGT).”

I don’t know what he is thinking, but my logic was that both the currency and the stocks are quite cheap; that natural resources are a good idea; that Brazilian companies are well placed to benefit from Venezuela reintegrating into the global economy, and that Brazilian interest rates have room to come down. None of these observations is particularly insightful.

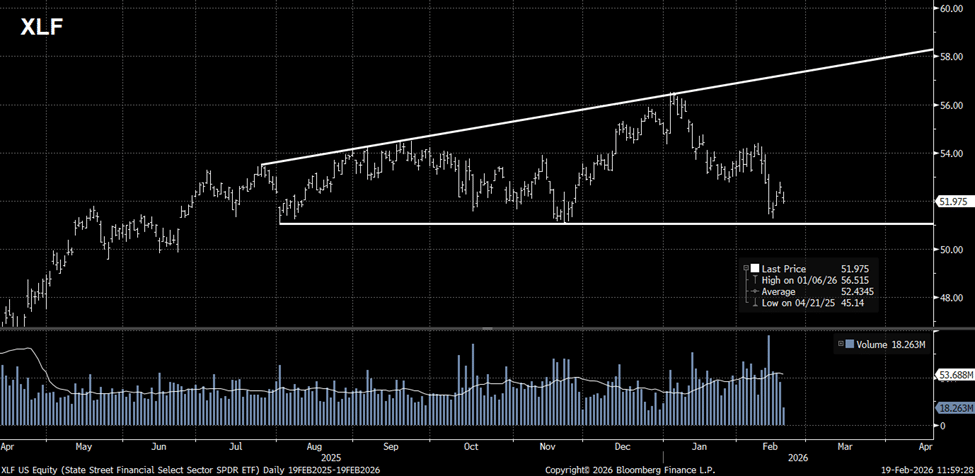

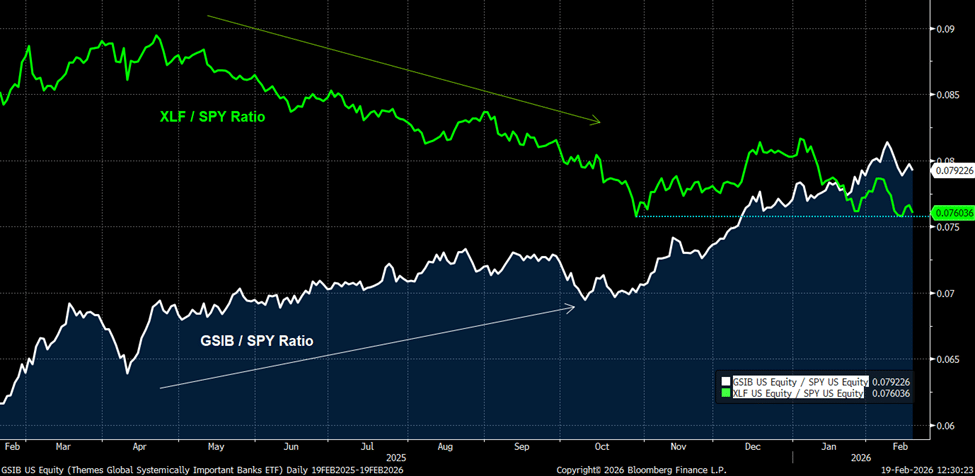

The other trade that caught my eye was his position in XLF. It struck me for two reasons: First, it seems to me that Warsh and Bessent’s position on the Fed’s balance sheet implies further relaxation of the prudential supervisory environment. Banks have been forced into a low RoE box that they could not escape. Bowman’s changes have progressively loosened those regulatory constraints and appear to have enabled banks to expand their balance sheets, which accommodate a significant increase in banks’ RoE. Bessent’s recent comments suggest that he is in no hurry to unwind what remains of the SOMA portfolio, which I take to imply that the order of events will be a) allow private sector bank balance sheets to expand first, b) then consider reducing the Fed’s SOMA portfolio, as and when the necessary reforms and backstop financing facilities are in place.

I very much doubt that either Bessent or Warsh has spoken to Druckenmiller about this for some time. But I would imagine that Mr D has a pretty good idea what they are thinking about these issues, and how they might approach the problem. The question came to mind because I came across this tweet. I agree with Mr Brandt: horizontal broadening patterns do often precede bearish outcomes (Mr Brandt is a very good classical chartist – I am not). That said, purchases by Mr D tend to work out. Another example of technical vs fundamental reasoning: in my experience, technical reasoning has been more reliable.

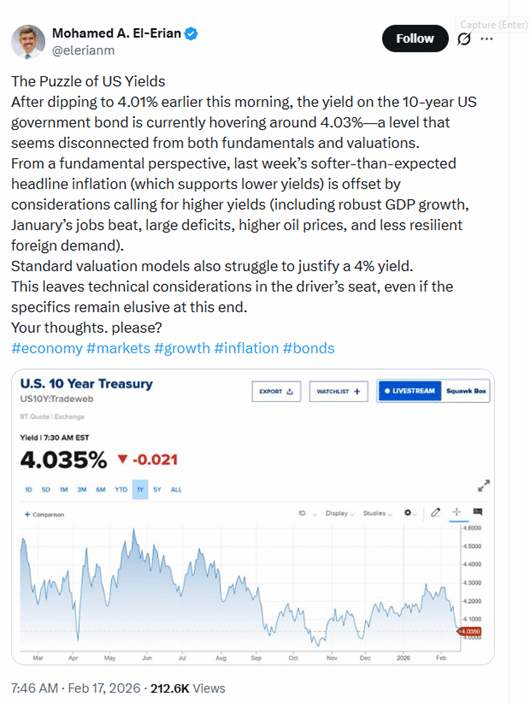

If you follow this Substack, you have probably gotten the impression that I think the environment has become rather hostile for private credit. Light-touch prudential regulation puts the banks back in competition with shadow banks. Funding conditions are getting progressively tougher, and there are some very high-quality names seeking very large sums for their AI buildout. So I was not surprised by the recent news about Blue Owl’s retail fund. You might remember the whole cockroach thing from a few months back. Mr Dimon’s “instincts” seem to have been on the money, and there is nothing like seeing investors locked into a fund they no longer want to encourage other investors to redeem. Let me be clear: one does not need to take a view on whether the underlying investments are “money good” or not. What I am saying is that the current investors wanted out, and Blue Owl couldn’t find enough new investors who were willing to take their place at current prices. This does not bode well, simply because most people are smart enough to redeem first and ask stupid questions later. So, when Mo El Erian asked this question, several possible answers came to mind.

- It’s possible that investors’ understanding of the Fed reaction function might have shifted with Warsh’s appointment. Might Mr Warsh take a different view of how “robust GDP growth, January’s jobs beat, large deficits, higher oil prices, and less resilient foreign demand” should feed into the optimal policy rate?

- Are macroeconomic conditions generally good? Has the economic data been unambiguously strong?

- Macroeconomic conditions are not the only factor to influence policy rates. Financial stability questions can affect them too. How much money has been lost in private equity/credit and CRE, and how exactly would realising those losses feed into the optimal policy rate decisions?

- Can the WH find other ways to keep its funding costs down and improve housing affordability? Are they already implementing those plans?

- Is any of this related to what Druck is thinking in XLF?

XLF bearish call spot on