I was tempted to write about the recent weakness in software stocks attributed to concerns that AI would eat their lunch, because the “SaaSpocalypse” is nigh: well, maybe. Of course, the real reason would have been that I could take one of my typically low-key “victory laps”. Quite a few of this substack’s recent posts have discussed this very possibility (Creative Destruction) and/or the vulnerability of private credit to the SaaSpocalypse (another favourite recent topic).

But instead, I will attempt to draw together three seemingly completely unrelated themes into a single coherent point (the substack equivalent of landing a triple axle). In part, this is because I have been long of precious metals (better lucky than good!) and the flash crash in PMs struck close to home. But also because I have some thoughts on the supposed backstory to the recent correction and what recent developments might tell us about policy and PM speculation going forward in both the US and China.

Rahm Emanuel once observed that “you never want a serious crisis to go to waste”. The idea is that crises are opportunities to achieve objectives that would otherwise be impractical. A number of commentators (and some very smart clients) had linked last week’s PM flash crash with the announcement that Trump had selected Warsh to be the next FOMC Chair. The idea was that Warsh was an inflation hawk, and Trump’s hawkish choice precipitated a rally in the dollar and the associated selling of PMs. I wrote about this last week, and I reversed the logic. Warsh is a Republican, and in his first stint at the Fed, he sensibly made very sure to burnish his inflation hawk credentials. But the idea that Trump would nominate an inflation hawk to replace Powell is wonderfully absurd, even if Anna Wong (among others) is prepared to carry that water. The administration has every incentive to present the violent price action as evidence of credibility. It isn’t that Warsh is an inflation hawk, but that given we had a PM flash crash, it would have been criminally negligent to waste the opportunity to sell him as such!

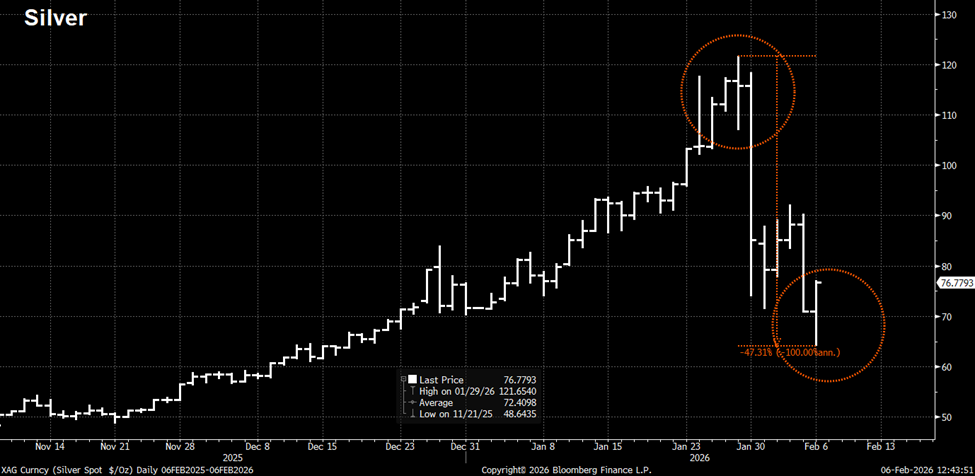

But if it wasn’t Warsh’s announcement that prompted the sharp repricing of PMs (and other metals), what was it? Well, the first obvious clue was Comex, rather predictably. increasing margin requirements. I asked a selection of AIs to verify that Comex raised margins just prior to the flash crash and was told (emphatically) that Comex only raised margin requirements after the silver price drop. This does not appear to be true, as suggested here, here and here. These links are not absolute proof (nothing on Twitter is), but they are strongly supportive. Besides, we don’t need proof that Comex raising margins precipitated the selling. Rumours would be more than sufficient, and I do think the links demonstrate that there was significant speculation of that. It is certainly not unusual for AIs to be wrong, but I was surprised by how emphatically they rejected the idea that higher margin requirements might have played any role in silver’s 30% flash crash. Curious.

The other rather striking element to the selloff was the rumours that JPM had managed to close their silver short at the lows. There was a consensus that this was proof of a dastardly conspiracy against the market, but I have a slightly different take. Over the years I misspent as a market-maker, I watched several situations where clients were liquidated by banks: Lehman liquidating its Russian repo clients in 1998 (yes, I am that old) is a particularly good example. The “optimal” approach is to sell out the collateral position very aggressively. Repo haircuts can be small relative to available liquidity, so one might argue the situation often calls for a “proactive” approach – “yours in your size, shag” “anything on the follow? Yours there too”. There is nothing to be gained by hesitation. You don’t have a duty of care to the client whose collateral you are liquidating, but to your employer, the bank that is at risk because the client has failed to make its margin call. The selling only stops when you get to the last 25% (or so) of the position, at which point the market-maker will often look to cross the balance with his own book, an internal “back book” or the bank’s “prop desk”. When you cross the balance will depend on how the market takes the selling. After all, the market-maker knows that the selling is now finished and there is a good chance that the market will bounce back. A lot of damage can be done by a prime broker liquidating a client’s position, although if the market is healthy, it will bounce back when the careless selling is done.

This scenario would explain the fact pattern we observed in silver: why JPM appeared to take a long position at the absolute low of the move: they were liquidating a client.

But has the silver market bounced back? Well, yes, but really no. It stabilized but it has not really come anywhere near regaining the old highs. Of course, that’s not entirely surprising when we consider the damage that might have been done to certain speculators. Pity Chinese retail accounts. Asian retail have been big buyers, but that flow does appear to have (at least temporarily) reversed. Surely that’s not down to JPM as well?

My suspicion is that we should pin the blame for this on the CCP. There was a very interesting speech by Xi where he laid out his vision of what a “modern financial system with Chinese characteristics” (中国特色现代金融体系) would look like. What was clear was that rampant speculation was not considered benign because it increased liquidity and so reduced the cost of investment for companies. Rather, finance should directly serve the people (well good luck with that!). The piece was widely covered in China, and thanks to Chatgpt I was able to read various translations of media commentaries. One commentary explained that Xi wants to “avoid the Western predicament of financial oligarchs hijacking public policy and deepening social division.” I am a “conspiracy theorist”, but am I wrong to link the flash crash in PMs with CCP officials’ distaste for rampant leveraged speculation in PMs? It’s one thing for SOEs to load their supply chain with inventories of strategic commodities, but quite another to have your households engaged in rampant PM speculation!

Speaking of “financial oligarchs hijacking public policy and deepening social divisions”, I was rather struck by how things have worked out for Stan Druckenmiller. Druckenmiller, probably the most successful speculator of his generation, now has two protégés in prominent government positions: one is the US Treasury Sec. and the other has just been nominated for FOMC Chair. Maybe it’s just me, but I do plan on spending a little time looking at all Stan’s recent interviews. It can’t hurt.

Finally, I feel obliged to comment on events in the UK and the trouble that Lord Mandelson has recently encountered. Trevor Phillips was given the honour of sticking the first dagger in (et tu Trevor?), and he did a terrible job of disguising his glee. Apparently, the world has just figured out that Peter might have traded information for money and favours. Imagine! Back in 2003, I had the “pleasure” of meeting Lord Mandelson. I was asked to walk him to Canal Street to help him find a cab. He was not particularly talkative, but I can tell you that he was taller than I expected and wore a very nice suit: my guess is it was a Brioni. It looked very good on him.