“Every new beginning comes from some other beginning’s end”

A few weeks ago, we talked about asking “why now?” as an analytical tool for understanding the Fed’s latest jawboning of Fed independence. The answer we suggested was a guess that Powell and friends were staking their narrative claim ahead of a potential clash with the incoming Trump administration. This week, we don’t feel the need to ask, “why now?” with respect to Yellen’s volte-face on the deficit. The queen of coo had previously argued that the deficit was nothing to worry about, when her day job was selling US debt. Now, facing a well-deserved retirement, she worries about the state of the US’s fiscal path. Cynics might view this as a case of the arsonist wishing that there were fewer forest fires, but is the thought of a consulting gig at a friendly shop (there are a few options) inspiring new honesty from the departing Treasury Secretary à la Richard Fisher?

“Tariffs are the most beautiful word”

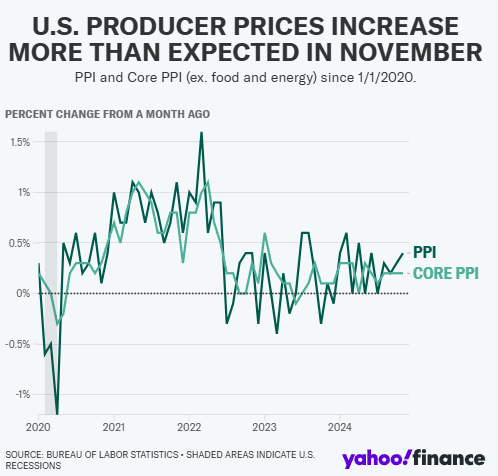

The easiest and most direct way to know Janet’s thoughts would be to take a look at her bond portfolio, but absent that data, is there something both Janet and markets are seeing? The long end of the curve has taken some heat over the last week or so, but, as far as the headlines give away, not for any particular reason. CPI ticked up slightly, but came in in line with expectations while PPI beat forecasts (to the high side) and saw “the highest year-over-year increase since February 2023”.

On the policy front, there didn’t appear to be any new tape bombs. Trump’s interview with Meet the Press reiterated his view of the benefits of tariffs, and inflation, and the president-elect even deescalated the rhetorical tit for tat with Chair Powell saying he had no plans to remove Powell. Does the bond market simply agree with Granny Yellen’s assessment, despite Trump’s plan via Scott Bessent to pull the deficit back to 3%? We remain somewhat sceptical, viewing fiscal as a sort of one-way ratchet, especially given that Trump’s ambitious industrial policy and foreign policy moves come with spending implications. But maybe…? In the meantime, we are reminded that the geographical shuffling of manufacturing comes with potential knock-on effects (see VW workers in Tennessee).

P.S. One of our favorite commentators, Warren Mosler, was back this week in an interview discussing the state of the US economy, the deficit, and why even though the Fed Funds rate has come back down, the federal government’s interest expenses are set to continue rising.