“There are several reasons why longer-term rates may have risen”

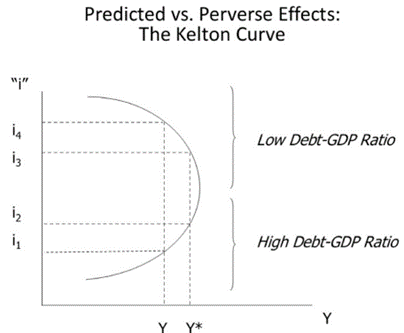

Larry Summers gave an interview recently positing that “interest rates may be less restrictive than they used to be”. Summers gave three examples to support this idea. First, with people locked (metaphorically) into their houses by high rates and inventories staying low, house prices go up, “and that makes people feel wealthier”. Second, with government debt at very high levels, as interest rates go up, “that’s more money in people’s pockets and they spend some of it”. Finally, when capital expenses are on AI, with low duration, there’s less interest rate sensitivity. Summers concludes that this will lead to more volatility in interest rates when “things need to be cooled off” and said this is an important part of the deficit and government fiscal position. Professor Summers noted that this year, the deficit as a % of GDP will rise by more than 3%, which he notes has “been a big push forward to the economy”—paging Mr. Mosler! That which was heresy is now being repeated by our most august priests. Providing more perspective on Summers’s second point, MMTer Stephanie Kelton, in a thread that included a retweet of Larry, cited the “Kelton Curve”, where under certain conditions, “raising interest rates could have perverse (i.e. expansionary) effects”, that is, as Mosler put it, they’ve “got it backward“.

As an aside, this reminds us of the various charts we shared back in the summer of 2019 when several commentators joined Mr. Mosler in wondering if received wisdom and assumed linearity might not be quite as reliable as many hoped.

If Professor Summer’s Damascene conversion was insufficient to surprise you, we also were struck by the thoughts of Lorie Logan of the Dallas Fed. Ms. Logan gave a speech which asked the rhetorical question of why rates had risen as much as they had. After concluding the first part of her speech by noting that she expects “that continued restrictive financial conditions will be necessary to restore price stability in a sustainable and timely way”, the Fed governor jumped into financial conditions, specifically that they had “tightened substantially in recent months” thanks to movements in longer-term interest rates. She then went on to “interpret the rate moves” and noted that “the rise in rates has come almost entirely in real interest rates”. Logan noted the rise may have been partially due to a rise in term premiums “that compensates for the risk of interest rate fluctuations”, which may be driven by “increases in the stock of debt relative to investors’ demand for debt”. Supply AND demand?! Related to this, and building upon Summers’s comments on government debt/deficit, all is well, according to Janet Yellen. As she said in a discussion at a conference this week, she is watching real net interest payments as a share of GDP and believes that over the next ten years, “the answer is 1%”, which is “historically completely normal”, based on the most recent budget forecasts. However, this relies on “meaningful deficit reduction over the next ten years”, and the projection has “three trillion of deficit reduction incorporated into it”. It’s almost as if one of her jobs was to finance the government. The IMF takes the other side of that bet, with a recent projection that the public debt ratio “would be above 140 percent of GDP by the end of the decade” compared to the 2022 figure of 110%. On the deficit front, the CBO is also less optimistic, with the latest Outlook saying the following: “In CBO’s projections, the deficit equals 5.8 percent of gross domestic product (GDP) in 2023, declines to 5.0 percent by 2027, and then grows in every year, reaching 10.0 percent of GDP in 2053.”

Growing every year, eh? Ours is not to reason why, ours is but to do and die.