“A Direct Cap on Long-Term Yields”

The FOMC convenes once again this week during a tempest. In addition to the ongoing international struggle to contain the corona virus and the potential knock-on economic effects (case in point, United Airlines has suspended a number of flights to China), there are signs of growing disagreement within the Fed. As a Bloomberg article discusses, Neel Kashkari took to twitter to mete out contumely to “QE conspiracists” just two days after Robert Kaplan said that “Not QE” is “having some effect on risk assets”. Kaplan warned that the Fed should be “sensitive” to its role in “elevated risk asset valuations”. Whether QE or not QE, the net liquidity provided by the Fed is set to slowly decline, with 14-day repo operation limits dropping from “At least $35 billion” to “At least $30 billion” at the start of February, while the parameters of the overnight repo operations and “Reserve Management Purchase” of Treasuries remain unchanged . In the meantime, markets are pricing in a roughly 88% chance that the Fed will keep its target rate unchanged, with the probability of a rate cut sitting at a round zero percent.

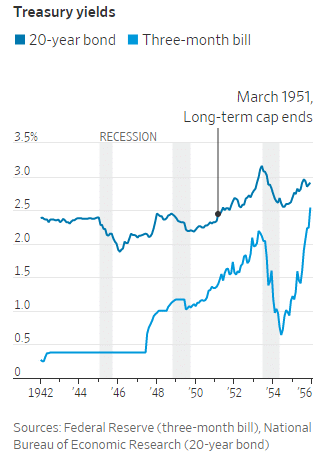

Beyond just the Federal Funds Rate and the current slew of open market operations, the Fed is also considering the sea of troubles it could face in the next recession. According to a recent article from Nick Timiraos in the Wall Street Journal, the Fed is looking at capping yields on treasuries “as part of their contingency planning for the next recession”. With Fed Funds sitting in a range between 1.5% and 1.75%, there’s little room for the Fed to cut, and the Larry Summer’s 5% would take rates well below the theoretical ZLB. As “Fed officials are unimpressed with negative rates”, other “approaches” are being studied. Last tried in the US during and after World War II, yield-curve control has been more recently used in Japan. A 2003 Fed Memo studying the Federal Reserve’s experience from 1942-51 provides some historical perspective. In addition to the all-too human elements of the Fed’s implementation (such as not formally announcing the cap in long-term rates, “perhaps to avoid embarrassment in case the policy proved unsuccessful”, the memo discusses some of the “important issues that arise”. An “exit strategy” was concocted to protect banks from “capital losses, which would in turn undercut the stability of the banking system”. There’s also evidence to suggest “that the policy may not have been entirely successful in holding down private-sector yields”. Finally, corroborated by Trump’s comments haranguing the Fed, the memo emphasized “scope for conflict between the central bank and fiscal authorities”.

“Consumers Will Continue to Drive Growth”

Following on the positive Retail Sales data we wrote about last week, this week’s Conference Board Consumer Confidence Index provides further evidence of the Consumer’s rude health. “Optimism about the labor market should continue to support confidence in the short -term” said Lynn Franco, Senior Director of Economic Indicators at The Conference Board. The Conference Board’s Leading Economic Index was less sanguine, declining 0.1 percent to 108.8, up just 0.1% YoY, “with the manufacturing indicators pointing to continued weakness in the sector”.