Geopolitics is one of our favourite distractions – rarely profitable, yet impossible for us to ignore. That’s why Lei’s analysis caught our attention. Her account elegantly solves two puzzles – just the sort of parsimony that appealed to William of Ockham: Why did China suddenly halt drone component sales to Ukraine, and why did Wang Yi become unusually candid about Beijing’s thinking on the Russia-Ukraine war? Her theory: a CCP defector turned up in Moscow with sensitive documents (and his superior’s wife!) outlining China’s contingency plans in the event of a successful regime-change operation against Putin and the installation of a Western-aligned Russian government. Putin’s response was a very tersely worded statement noting that Russia was a nuclear power, and the return of both defector and wife. Lei’s theory is that the deepening mistrust between Moscow and Beijing created an opening for Trump to drive a wedge between them, prompting Beijing to respond with tangible support.

But there is a broader lesson here, beyond the very real dangers of eloping with your boss’s wife. Sudden bouts of honesty are often suspicious developments which can signal ulterior motives. Lei suggests that Wang Yi’s uncharacteristic “honesty” was not addressed to Kallas and the EU but to Putin and Moscow and sent a signal of its commitment to the bilateral relationship. Maybe.

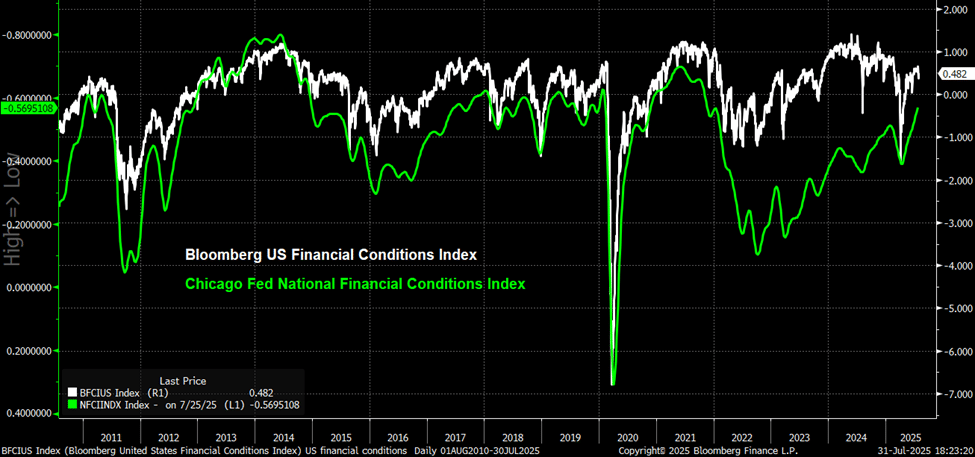

All this came to mind when watching Chairman Powell’s post-FOMC presser. The meeting was noteworthy for several reasons. First, both Trump appointees dissented from the decision to hold rates steady. While not unexpected, it was unusual, as the first double dissent since 1993. The WH has made no secret of its preferred policy mix, and would no doubt appreciate Bowman and Waller’s efforts to lock the Fed into a September rate cut. Equally, Powell would want to resist attempts to limit his freedom of manoeuvre, and his comments at the presser were very effective in dissuading rate markets from pricing September as a done deal. We were particularly struck by a comment Powell made around the 11:30 mark: “You could argue we are (a bit) looking through goods inflation by not raising rates”. That, combined with his “ye shall know neutral through its works” suggested that while Trump might want lower rates, the best the Powell FOMC could do was not raising rates against a backdrop of accommodative financial conditions and stubborn headline CPI. After all, look at financial conditions!

Powell’s honesty might have settled matters for rates traders, but it was unlikely to have won friends on Pennsylvania Avenue. Joseph Wang pointed out that some might think the Fed already politicised. There does seem to be some singing from the same Project 2025 hymn sheet.

One plausible reason why Trump might be so keen to see the policy rates lower is that fiscal conditions are about to take a turn for the worse. Bob Elliott took a tour through the fiscal outlook, concluding that we were likely to see “a big negative shock in the near term, gradually easing starting 2H26”. In the circumstances, Trump might have perfectly sound reasons for wanting the Fed to ease the monetary conditions pre-emptively. After all, it would be a shame if the Fed were late to ease and cause the Trump mini-boom to peter out. Not that we have any doubts regarding Powell’s integrity, but we can’t help but think Trump and co do.

Honesty and transparency are not synonyms. British civil servants were masters of the distinction and considered the art of misleading while telling the literal truth integral to their craft. Which is why increasing concerns among economist-types regarding the quality of economic statistics are more interesting than they sound. 30% of the CPI is now imputed, up from 10% not so long ago (OER is the most obvious example), and some of the results of the imputed components seem counterintuitive. Which means it isn’t clear whether Trump or Powell is “right”, whatever that means.

The combination of honesty and transparency in government (particularly the Fed) is particularly rare. Of course, there are some excellent reasons for that. But that doesn’t mean there aren’t also some bad reasons for it. David Andolfatto points out that “raw transcripts without context risk misinterpretation. They might generate more noise than signal, especially when viewed through a partisan lens.” But “raw transcripts without context” also risk observers reaching the “correct” interpretation, which might generate a little too much signal, especially when your political adversaries can see what you are doing.