Some might think it academic, but we can’t help being curious about who blinked first. There are at least two games of chicken we have been closely watching. Clearly, everyone is watching the game of chicken between Xi and Trump. However, the casual observer might think there was also one involving Powell and Trump. In the case of Xi, its not entirely clear who blinked first.

Perhaps we dreamed it, but we had the impression that the Chinese required unilateral tariffs to be cut before they would agree to even discuss a trade deal. “When asked why China now appeared open to trade negotiations—after previously demanding tariff removal as a precondition—Lin said there had been “no change” in China’s position.” Maybe, but the S&P500 clearly thinks there was a change. After all, if there was no change in China’s position, why would Bessent and Greer go to Switzerland, and who would they meet with?

There is scope for disagreement here, but there is no mistaking the sense of optimism from bulls, particularly the Equity Bull in Chief. “You better go out and buy stocks now,” Trump said. “Let me tell you, this country will be like a rocket ship that goes straight up.” Currency traders completely agreed, and the dollar rallied across the board. The only sour note came from the bond markets (typical!), which had a stinker across the curve.

Which brings us to what might appear to be the other game of chicken. We have already expressed our doubts that Powell’s job was ever really under threat, but if it was, Powell does not appear to have been at all concerned by the President’s claim that he was making a (policy) mistake by dragging his feet. “Uncertainty about the economic outlook has increased further,” officials said in their post-meeting statement, the first since President Trump imposed sudden tariff increases last month. “The committee … judges that the risks of higher unemployment and higher inflation have risen.” It’s easy to agree that uncertainty is higher, but it’s not exactly a gimme to say that means the Fed should do nothing. Oil is down, as is consumer confidence, and both the ECB and BoE came to different conclusions. Waller suggested that second-round effects from higher inflation were likely muted, although that might be what he thinks his potential future boss wants to hear.

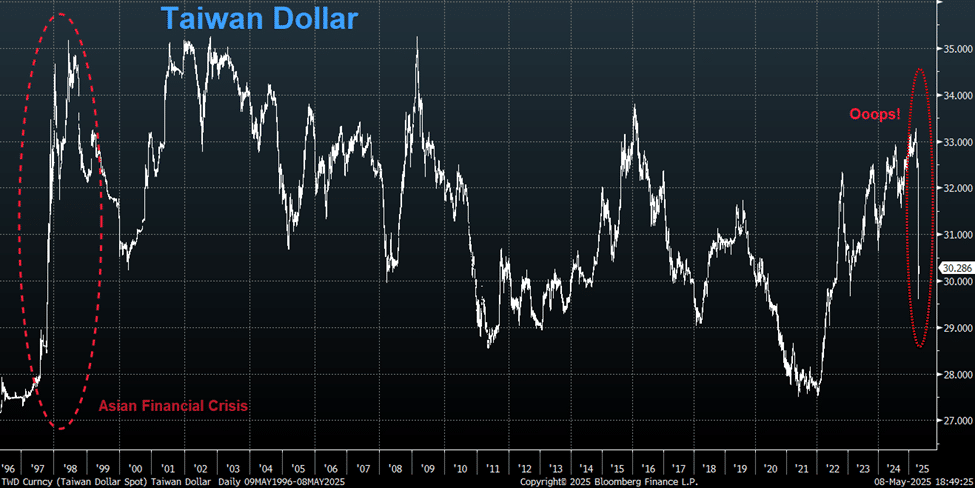

We doubt that Trump ever intended to fire his scapegoat, especially considering his term ends in 12 months. Besides, with bonds looking so sickly, firing the Fed Chair is probably not even good for stocks. One wonders how much stocks can rally if bonds keep trading this badly. And that’s without considering how the appetite for (unhedged) dollar bonds has been affected by the shocking move in the Taiwanese dollar. Forgive us if we take a victory lap, but even Larry Summers is now singing from our hymn sheet. Taiwanese investors were the proud owners of around $700bn dollar-denominated bonds, of which at least 70% were unhedged. Buyers remorse?