“The Federal Reserve is independent from politics. That doesn’t mean that politics is independent of the Federal Reserve.”

The ECB cut rates another 25bps as expected and explained in its policy statement that the “outlook for growth has deteriorated owing to rising trade tensions…Increased uncertainty is likely to reduce confidence among households and firms, and the adverse and volatile market response to the trade tensions is likely to have a tightening impact on financing conditions.” Adding that “the disinflation process is well on track.” Madam Lagarde understood exactly which risks should be prioritised, and there was no discernible controversy surrounding the ECB decision. Further rate cuts are expected.

Back on Sep 18th, 2024, TFTD (“More Cowbell”) featured the above quote from the NYT’s Jeanna Smialek. Her comment was telling in two ways. First, as a reminder that while central bankers might wish they were above the swamp (that is politics), that won’t stop the swamp creatures coming to get them. Second, can we be sure that ALL central bankers want nothing to do with “wetlands”? We are all subject to bias, and the problem with subconscious or subliminal bias is that it can be very hard to detect.

That said, the bias that concerns the WH does not appear to be subtle.

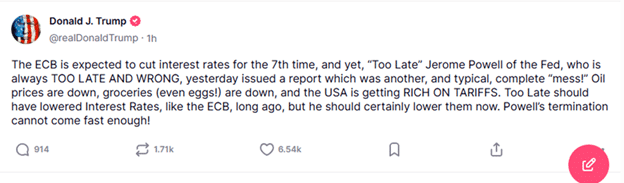

Ignoring questions of who is at fault for the “rising trade tensions” (let’s not play the “blame game”), it is clear that Trump thinks the current policy mix inappropriate. We were particularly struck by Trump’s capitalised “TOO LATE AND WRONG“, which seems to be the essence of WH messaging. However, Jerome Powell’s recent comments at the Economic Club of Chicago suggest he disagrees about the balance of risks. “For the time being, we are well positioned to wait for greater clarity before considering any adjustments to our policy stance,” Powell also noted the possibility of a tough situation developing for the Fed: one in which inflation is pushed higher by tariffs while growth and employment weaken (don’t use the S-word!). Worse, when asked whether there was a “Fed put”, he replied that markets were “orderly, and they’re functioning just about as you would expect them to function”.

The 2.2% decline in the S&P 500 suggests that equity investors didn’t care for Powell’s tone, and one might think further weakness in stocks would only increase the threat that Trump “terminates” Powell. Reuters hinted that it was only Bessent’s intervention (who were Reuters’ sources?) that saved Powell (and the bond market), presenting the story as Bessent’s “good cop” to Trump’s “bad cop”. But Politico offered a more nuanced framing: “White House allies see Trump’s Thursday morning post less as an attempt to immediately oust Powell and more as an effort to throw the Fed chair off balance and position him as a future scapegoat for the country’s economic woes. The post also seems aimed at increasing pressure on Powell to capitulate.” We can see why Trump might try to create facts on the ground in terms of rate cut pricing while increasing the stakes for Fed officials. James Goldsmith once said that the problem with marrying your mistress is that it creates a vacancy, and so it is for Trump. What’s the point of firing your scapegoat? You will just create a vacancy. Expect the simultaneous games of blame and chicken to continue. After all, what could go wrong?