Last week, we briefly discussed the Tricolor collapse, not because we are particularly worried about deteriorating US credit quality, but rather because we wondered whether it might be a pointer to any “collateral damage” associated with Trump’s reversing US immigration policy. First, a quick reminder of the FT article that piqued our curiosity.

(h/t to Alex J, who was kind enough to point out many flaws in my arguments).

To our jaundiced eye, this looks like an adaptation to economic incentives: the question is how pervasive this kind of economic adaptation was, and to what degree did it skew the macro data? If it was sufficiently sizable, its reversal (to the extent that ICE succeeds in its job) might be expected to be of a roughly similar order of magnitude (“roughly” is doing a lot of work here!). An example might be used car prices. We know that supply chain issues were the major cause of the COVID spike in used car prices. What we don’t know is how much of the demand side might have been impacted by demographics like Tricolor’s customers. It’s worth noting that used car prices were tightening again as recently as July (tariffs?), but the latest results from Car Max suggest that might no longer be the case.

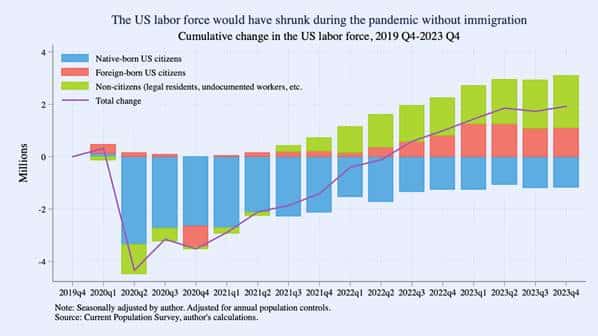

One approach to thinking about the question of scaling the economic impact is to estimate how much migration contributed to US growth in recent years. We have looked at this question before (TFTD: “Regrets”). Brookings did a piece which suggested that migrants (foreign-born citizens and non-citizens) had boosted the US labor force by about 3 million between Q3 2019 and Q4 2023. That implies we needed about 200k jobs per month to keep up with labor force growth, and if we lost them, we might need 100k fewer jobs created. Tedeschi wrote a useful paper estimating the potential impact in terms of GDP. He estimated that of the 8.2% real GDP growth since Q3 2019, 1.6% (or about 1/5 of the total growth between Q4 2019 and Q4 2023) could be directly attributed to immigration (legal or other). Since this estimate ignored indirect effects (e.g. innovation, spillovers, etc.), it’s likely on the low side. All the more so, since the guestimates in Tedeschi’s piece were based on the Current Population Survey (a joint production of the Census Bureau and the BLS), and it’s possible the CPS were underestimating the scale of illegal immigration.

Given the excellent job ICE is doing, it’s obvious illegals will make a far smaller contribution to the US labor supply going forward. But how much smaller? Yes, there is the risk of extended detention followed by repatriation, but won’t migrants need to work to survive despite the risks? Will they not eventually have to just suck it up? Given Tedeschi and Co.’s analysis, we can put numbers on the maximum order of magnitude (sadly, we feel obliged to show these to paid subscribers first), but we still need to guestimate the time frame over which labor supply would be reduced.

In practice, our best shot at estimating the scale of the macro effects is most likely to come from micro evidence, i.e., corporate results. We suspect that migrant labor would have been a significant tailwind for companies like DoorDash or Uber. So, one possible clue as to how big the contribution of migrants was to recent US economic performance is likely to come from their corporate results. We are also keeping a close eye on Carvana, cos of anecdotes suggesting used car demand might have been boosted by foreign-born legal citizens, subleasing multiple cars to illegals. As Alex pointed out, surely DoorDashers would prefer to use the cheapest cars they could find, rather than Carvana’s relatively pricey products? Probably, but perhaps the main constraint was underwriting standards rather than cost?

Finally, the anecdote that prompted this screed: rents in Boston are lower. It’s been reported that one factor behind this is that fewer foreign students are coming. But local real estate brokers have reported to us that while the local news has yet to notice, areas with heavy immigrant populations are also experiencing significant downward pressure on rents. Those landlords face multiple threats, some of which are worse than tenants that disappear in the night: Trump has shown interest in Section 8. What will happen if tenants disappear, but interest rates don’t come much lower?

P.S.

MI2’s Harry Melandri hosts a must-listen conversation with Andy Constan, founder of Damped Spring Advisors, covering everything from Fed decisions and market mispricings to the housing mechanics and policy risks. Clear macro insight, sharp takes—don’t miss it!