“We have not seen clear progress”

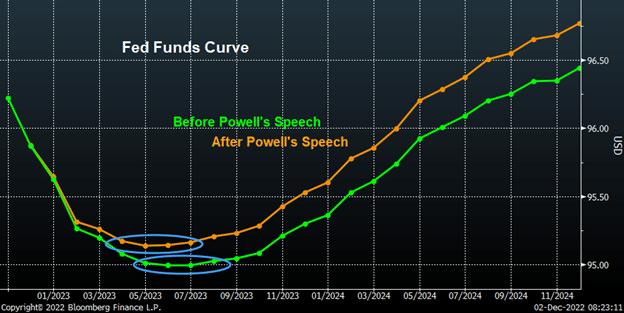

While this section’s title may evoke a sense of déjà vu, it is hot of the presses from Jerome Powell’s latest speech. His talk on “Inflation and the Labor Market” came with several hawkish quotes, including “by any standard, inflation is too high”, “I will simply say that we have more ground to cover”, and concluding with “It is likely that restoring price stability will require holding policy at a restrictive level for some time. History cautions strongly against prematurely loosening policy. We will stay the course until the job is done.” Perhaps “stay the course” is the new Fed mantra? The speech did, however, also contain the admission that a moderation in the pace of rate increases is on the horizon, which headlines cited as the “spark” to Wednesday’s “massive stock rally”. Rates markets also moved following the speech and looking at the before and after snapshot of the Fed Funds curve, the market priced in both a lower peak in Fed Funds and less time hanging around at that rate before the Fed starts to cut.

“The darkening outlook for demand”

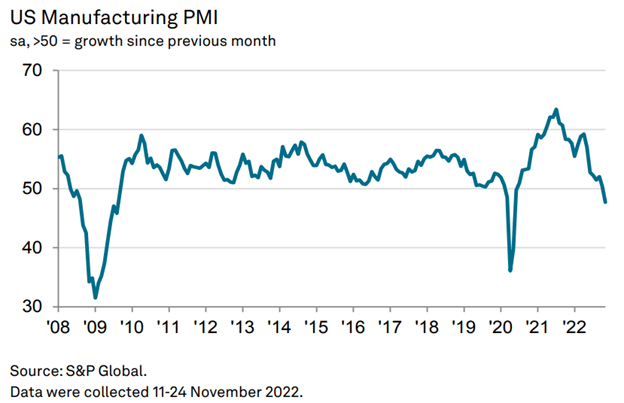

The latest manufacturing data was flashing red warning lights in the background this week. On the regional side, Dallas started the week by beating expectations, but the report’s headline noted that though manufacturing activity was flat, “outlooks continue to worsen”. Meanwhile, the Chicago PMI fell “deeper into contraction territory” and missed estimates significantly. However, it was the national data that most clearly warned of trouble ahead. S&P Global’s US Manufacturing PMI “signalled a renewed deterioration in operating conditions,” and comments from Chris Williamson, its Chief Business Economist, highlighted that “even with the latest production cuts, the downturn in demand has still led to one of the largest increases in unsold stock recorded since survey data were first available 15 years ago”. Moreover, “companies are slashing their purchases of inputs and raw materials” as “the business mood remains among the gloomiest seen over the past decade”. Tim Fiore at the ISM was less dour. While the headline number did come in at a contractionary 49, his adjectives weren’t quite as piquant, “panelists reporting softening new orders” and the manufacturing sector “dipped into contraction”. The milder adjectives are perhaps appropriate given the ISM saw dynamics similar to those reported by the S&P but on a more muted scale. Customers’ Inventories jumped by the largest amount since 2015 (admittedly climbing into “‘just right’ territory”), and Inventories continued to grow for the second month in a row (with the caveat that they grew slower than in October). The ISM report did, however, contain a “very small but a distinct warning” in its Employment data. While the Employment index itself only dropped from last month’s neutral level of 50 to 48.4, Fiore noted that there was a shift, “companies confirm that they are continuing to manage headcounts through a combination of hiring freezes, employee attrition, and now layoffs”. The emphasis is our own, but Fiore’s comments don’t come as a surprise, at least given what has been happening in the tech sector and the data from the NFIB. This may be welcome news to Powell and the Fed, who are looking for a “restoration of balance between supply and demand in the labor market“, but the shift in Fed Funds, rather than being a tug of war between hawks and doves, could be the market saying that perhaps Powell and company won’t be able to stick to “holding policy at a restrictive level for some time”? As noted in regard to the housing market, sometimes arriving at the point of balance is not always a painless process.

“Worry about the potential long-term impacts”

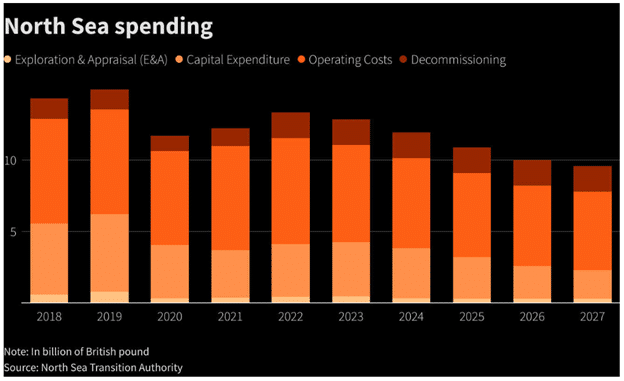

Though headlines had trumpeted that Europe’s natural gas storage was nearing capacity and there was some optimism that the energy woes of Europe and the UK could be seeing some form of denouement, it’s too early to count the chickens (or turkeys?). Sure, there have been some positive developments in the form of the approval of “new investments” in Norway’s North Sea petroleum fields “, which will boost gas exports to Europe from 2026” and Germany is set to get new gas flow from Qatar starting in 2026 thanks to a recently signed long-term contract (following in China’s footsteps…?). However, these moves will take a few years to yield any substantial change. In the meantime, many energy producers (Total, Shell) are backing off from investing in the UK, courtesy of the windfall tax (previously scoffed at by the short-lived Truss administration). What’s more, while there have been several different schemes proposed to alleviate the pinch of high gas prices, the CEO of British Gas’s parent company has discussed how the structure of the scheme, specifically that gas companies receive payment upfront, may not save companies from going under, and if things go wrong, “our customers have to pick up the cost”.