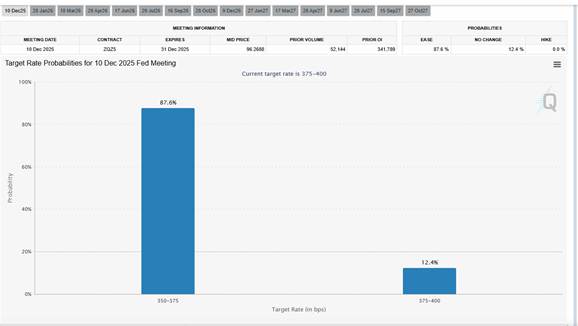

Since William’s speech on the 21st November, the market had come to understand December was a done deal. It wasn’t just Williams’ reincarnating into a dove. We also had some weaker labor market data, in the form of ADP, Intuit, and JOLTs. It wasn’t difficult to discern weakness in any of those series, so it wasn’t particularly surprising that short-rate futures markets priced an 87.6% probability of a 25bp cut on the morning of the 10th.

So why did precious metals and risk assets in general rally if the outcome was discounted? Part of the answer was in Powell’s Q&A. The consensus leading into the meeting was that it would be a “hawkish cut” (oxymoron?).

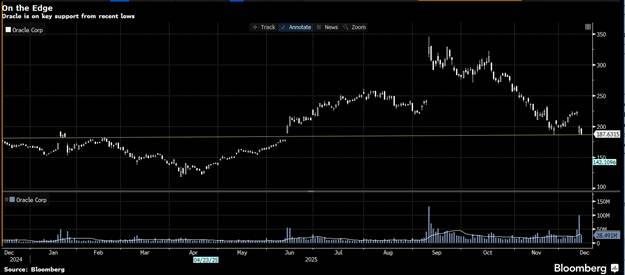

Now one might ask precisely how a “hawkish cut” is defined. Well, one answer is that it might involve hawkish dissents (check). It might also involve a “dot plot” showing very limited expectations for future rate cuts (check – excluding Miran, of course). What it probably does not involve is a sharp rally in precious metals and stocks (excluding Oracle, but we will come back to that) or a sell-off at the long end of the curve.

So, what went wrong? Well, Jeff Snider pointed to the data. And for those interested enough to watch the Q&A (or read it), that answer has the advantage of being consistent with some of Powell’s comments. Powell was not hawkish, and that wrong-footed the market. Perhaps he is bad at “message discipline”, or perhaps it’s the audience (us) that couldn’t grasp the subtleties of FOMC “risk management” or “insurance cuts” in Nick Timaros’ words (page 5). Regardless, it’s hard to completely free yourself of the notion that we might have to recalibrate our Fed “reaction functions” towards dovish.

That was not the only popular talking point which came out of the FOMC. Much attention was paid to changes in the Fed’s reserve management. Some reports framed it with reference to the recent end of quantitative tightening, which I took as a way of saying that the Fed might have taken slightly too many reserves out of the system, given certain seasonal demands (like tax season). In practice, what was announced was that the Fed was going to buy $40bn T-bills today. What followed was a frenzy of connecting dots on social media. Was it the starting of the “brrrr printing press”? Is Bill buying a gateway drug for QE?

Well, we think this is a more nuanced question than some. Certainly, Fed actions point to a (temporary) shortage of reserves in the system. NY Fed’s John Williams met with primary dealers in mid-November, to discuss the Standing Repo Facility. My guess is that the Fed was puzzled why primary dealers don’t want to tell their counterparties that they are struggling to borrow on good terms (btw, Roberto Perli is a top-notch thinker!). So, the reserve management exercise might be the Fed’s way of easing what it perceives as a little short-term funding stress in the system. Others were even more sanguine. While I generally find myself in agreement with Bob, I would note that if there aren’t enough reserves in the system with a $6.13 trillion Fed SOMA portfolio, then perhaps the banking system isn’t as well capitalized as it could be. If nothing else, it certainly doesn’t signal a steely-eyed focus on harsh monetary discipline, but I don’t suppose that’s really news to anyone.

The reason the equity market didn’t gap higher with PMs on all the “good news”, was because Oracle’s results were a little disappointing. Apparently, revenue growth missed expectations while spending on AI infrastructure surged, raising concerns about profitability and sustainability.

One might consider this a problem for investors who are all-in on the AI story. After all, if Nvidia’s clients are not making money, one might question how much longer they will keep buying Nvidia’s products. There are all sorts of corollary questions, if you think AI-related wealth effects might have been propping up consumer spending of late. But it’s not the kind of ill-wind which blows no good. If you are an active manager of equity portfolios, it’s a godsend! From massively underperforming passively managed products (due to those pesky stock concentration limits), they now get a chance to claw some relative performance back, just in time for bonuses. So, they have that going for them. Which is nice.