As the GFC made glaringly apparent, the state of the US housing market is a critical link in the overall U.S. economy, and one of the metrics we like to watch, as mentioned (here). The Fed is also watching the housing market because housing prices, like the stock market, are part of the wealth effect, where consumers feel cash-flush and are inspired to spend. The Boston Fed’s Raphael Bostic is intimately familiar with this dynamic, having published a paper in January 2007 discussing the relationship between housing prices and personal consumption, finding that from 2001 to 2005, increasing real estate wealth accounted for more than 12% of the growth in personal consumption expenditure or 9% of U.S. GDP growth during that time. However, as the paper notes, the wealth effect is a double-edged sword:

“Those same computations suggest the possibility of sizable reverse wealth effects in the context of a retrenchment in house values.”

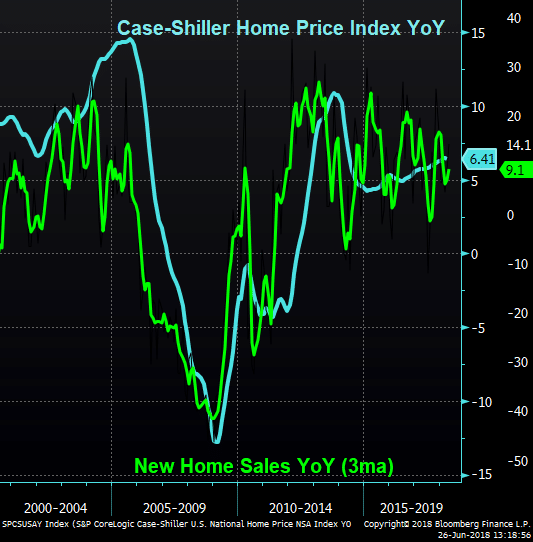

While the Case-Shiller Home Price Index isn’t showing significant weakness, with the recent reading of 6.56% YoY coming in slightly below expectation, and New Home Sales surprising to the upside, the anecdotal evidence regarding the broader category of shelter is mixed. On the one hand, certain localities are experiencing significant softness, as discussed in this article regarding the Seattle rental market, where supply is catching up to demand and landlords are offering everything from free months to Amazon gift cards. On the other side of the equation are reports, such as the one coming from Lennar, the US’s largest home construction company, that things continue to go well,

“[S]trong results were supported by continued solid fundamentals in the housing market… Concerns about rising interest rates and construction costs have been offset by low unemployment and increasing wages, combined with short supply based on years of underproduction of new homes.”

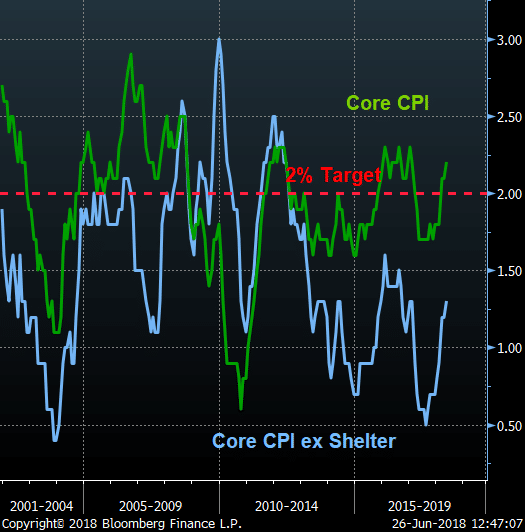

And while the consumer may be inspired by higher home prices to open the spending spigots, not everyone is so pleased about shelter inflation. According to a Bloomberg article (monthly article limit), later this week, a paper by Dean Baker from the Center for Economic and Policy Research will be presented to Boston Fed’s Bostic to show how shelter costs are interfering with the signal the Fed is receiving from Core PCE, with the problem that “most sectors of the economy are seeing a real interest rate that is considerably higher than the core inflation rate implies”. Additionally, Baker states that “If shelter costs are removed from core measures of inflation there is zero evidence of any acceleration in the inflation rate”, arguing that “The rapid pace of increase in shelter costs is not due to rising construction costs, but rather due to restrictive zoning practices in a limited number of highly desirable metropolitan areas that have limited the supply of housing”.