Subscribers will not have been surprised by the return of the tariff monster. In our June Research Dossier, “When Fiscal Dominance Met De-Globalization” we wrote,

“In essence, Trump’s team decided that the correct sequencing involved getting the Big Beautiful Bill (BBB) deal across the line before subsequently circling back to tariffs. Doing it in this order prevents Congress from tying support for the budget to tariff special pleading, giving the Trump team much more freedom of manoeuvre. Moreover, the massive fiscal stimulus (CBO) implicit in the BBB presents an implicit case for budget hawks to reverse some of the fiscal damage with tariffs.”

The One Big Beautiful Bill Act was signed into law on July 4th. Trump didn’t waste any time getting his tariff mojo back on track, but the newly announced Brazil tariffs had a lot of market folk scratching their heads. The US runs a trade surplus with Brazil, and while freedom of speech is evidently dear to the President’s heart, it’s stretching credulity (sad face emoji!) to imagine that he is punishing Lula for his anti-X policies.

So, what is Trump trying to achieve? Some suggest it is about negotiating leverage, although given Brazil’s trade deficit with the US, it’s hard to believe the ultimate WH objective is “fair trade”, whatever that is. Rather, the administration’s policy is aimed at reshoring industrial production, which has nothing to do with “fairness”. However, in this case, even that explanation makes little sense. Brazil does not export industrial goods to the US; it exports commodities, and regardless of what Trump does, he is unlikely to persuade Brazilian farmers to relocate their coffee plantations to the US. Sometimes, policies have a broader, more important purpose than initial impressions might suggest. In this particular case, we were struck by the coincidence of Lula hosting the BRICs summit and Trump’s singling out Brazil for special treatment. Perhaps Trump figured that the BRICs might benefit from seeing the risks of conspiring to reduce reliance on the US dollar in international trade? “Pour encourager les autres”, as Voltaire said. This view was subsequently confirmed by Lula. The Brazilian also said countries like his are not obliged to continue using the dollar to trade, reiterating remarks he made at last weekend’s BRICS summit in Rio de Janeiro that he acknowledged “likely worried Trump.”

The problem with this is that because Brazil doesn’t sell much to the US, it doesn’t cost Lula much to ignore Trump’s threats. To be exact, trade with the US is about 1.7% of Brazilian GDP. And Trump isn’t the only leader who can get a polling boost by wrapping himself in a flag , even if “MBGA” doesn’t exactly roll off the tongue. Ironically, if Brazil has a trade problem with anyone, it’s with China. China has been rapidly increasing its direct investments in the Brazilian economy. And while Brazil currently has a big bilateral surplus, Chinese-manufactured exports are growing. Chinese EVs have been flooding the Brazilian market, perhaps reflecting China’s recent pivot away from the US. That will be scant comfort to Brazilian automakers, which are subsidiaries of multinational autos.

It probably isn’t very comforting to US companies either. Tariffs are already squeezing corporate margins, even if the stock market doesn’t seem that worried. John Authers tells us that if tariffs go ahead as announced, then the average tariff rate on US imports will be at its highest since Smoot-Hawley. Ernie Tedeschi suggests an effective tariff rate of 18% and that it will cause an effective CPI bump of 1.8%, assuming no Fed reaction (i.e. Waller gets the nod). In the circumstances, it’s easy to see how attempts to coerce dollar use among BRICs could backfire faster than Reed Smoot leaving a speakeasy raid. It’s not as if the US long end has so many global admirers right now, and a series of nasty CPI prints is unlikely to improve that. We found Stephen Miran’s argument less convincing than we had hoped. “Sure, it’s possible that Bears sh*t in woods, but other things are possible too”. That’s not exactly a refutation.

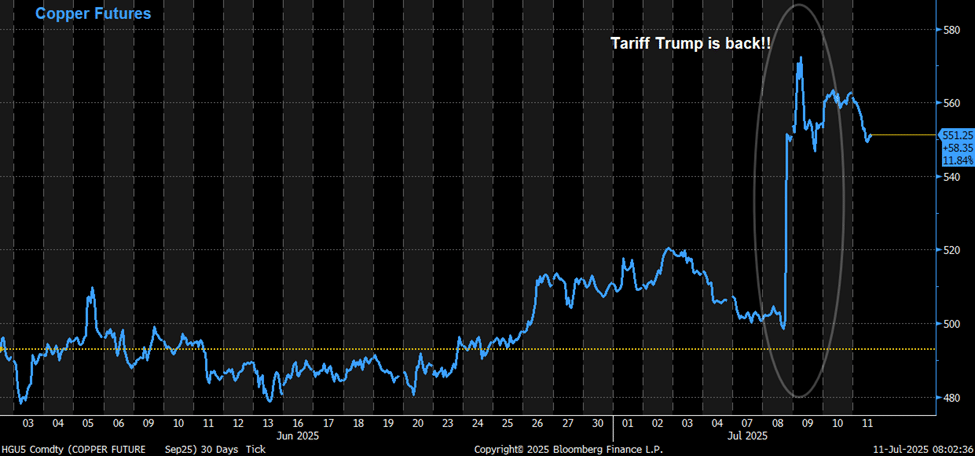

Of course, true believers in TACO will be unconcerned. Alternatively, some might believe that other countries will chicken out. However, unlike foxholes, there appear to be few true TACO believers in copper futures markets.