Paul Tudor Jones knows a thing or two about markets, so when he speaks, we listen. In a recent CNBC “Squawk Box” interview, Jones said that “all the ingredients are in place for some kind of a blow off… History rhymes a lot, so I would think some version of it is going to happen again. If anything, now is so much more potentially explosive than 1999.”

Of course, much of what Mr. Jones says is in line with our thinking. Specifically, that the current setup bears an uncanny resemblance to the “setup leading up to the burst of the dot-com bubble in late 1999, with dramatic rallies in technology shares and heightened speculative behavior. Jones said the circular deals or vendor financing happening in the artificial intelligence space today also made him ‘nervous.’”

The situation makes us “nervous” too, but it’s probably too early to do more than take a seat a little closer to the theatre exit. This point was echoed by Michael Hartnett (like us, another old fart), whose last “Flow Show” was titled “Krunchy Kredit”.

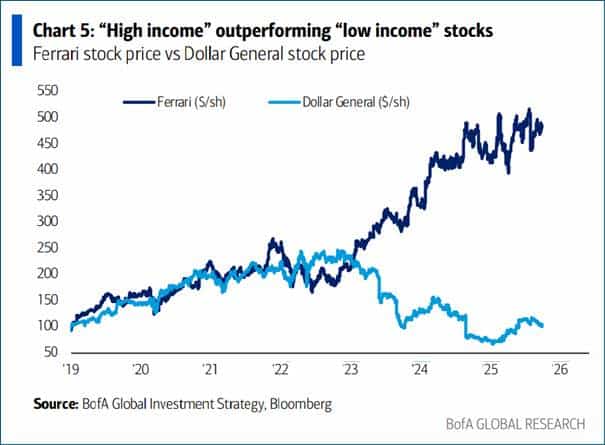

We guess the title reflects the apparent “cracks” that are beginning to show in corners of subprime credit markets. Hartnett referenced the apparent “K-shaped” US economy, which isn’t entirely surprising when stocks are making a string of new all-time highs: People don’t spend their capital gains in Dollar General.

The “cracks” Hartnett referred to are currently confined to some very specific market niches. Our working hypothesis is that the problems in subprime auto lending (Tricolor) are at least partially related to ICE’s crackdown on illegal migrants. Apparently, Tricolor is having trouble locating 30k vehicles, which it lent against. There are several possibilities, but we would like to offer a suggestion.

As we noted in a previous TFTD, Tricolor is not the only evidence of stress in the auto industry. CarMax’s most recent results were disappointing, and First Brands has recently sought protection from its creditors. Of course, there is a (tenuous) connection via autos, but while we regularly apply Occam’s razor, sometimes events are not directly, but rather indirectly, linked. In this case, the common link might be WH policy. Turfing out illegal migrants was always bound to have collateral effects (sorry), but we do not remember seeing anyone suggest the effects would manifest in subprime auto lending, or businesses like CarMax, both of which may have previously benefited from migrant demand for used autos.

That was not true with respect to tariffs. Some people did suggest that tariffs would place additional pressure on working capital, with possible collateral effects on corporate solvency. Low-margin businesses, with high credit needs, are always quite close to bankruptcy. And adding tariffs to the working capital requirements of businesses who have already stretched financing could easily be the straw that broke the camel’s back. Either way, these bankruptcies spell trouble, both for creditors (good luck finding those 30k cars, amigos) and for consumers. Still, the restructured businesses are likely to have much better margins, so it’s not all bad news.

Which brings us full circle back to the concerns various “old farts” (such as ourselves) have about the AI boom (by the way, it’s great to see Andy Constan back on X). Low margins are not usually consistent with high multiples, but that’s what we have right now. In a tiny pointer to potential vulnerabilities, The Information published a story about leaked internal Oracle documents pointing to much lower margins on its AI cloud business than analysts had assumed. The Information is pay-walled, but Yahoo were “kind” enough to cover their story. Oracle generated $900 million from renting Nvidia-powered servers in the three months to August, generating a gross profit of just $125 million. That translates to a rather uninspiring 14% gross margin. That 14% gross margin took account of most costs but only some of the depreciation expense. Additional depreciation expenses would reduce the margin by another 7%.

Which is why we find ourselves regularly asking who might be suffering from confirmation bias? Could it be the “old farts”, or is it the market?